Tessenderlo

15-20% ROIC business trading at only 9x earnings

Debt free by 2022

Headed by Luc Tack, one of smartest operators and capital allocators in Europe

Tack is aggressively buying shares

Significant tail winds for most business lines ahead

What got me interested in Tessenderlo is Luc Tack and his track record with Picanol. Picanol sells weaving machines to the textile industry, and was basically a mismanaged family run company. It never seemed to make much profit and in 2009 Luc Tack took a controlling stake in the company for about €3 per share, and turned the company into a profit machine without really having to significantly increase revenue:

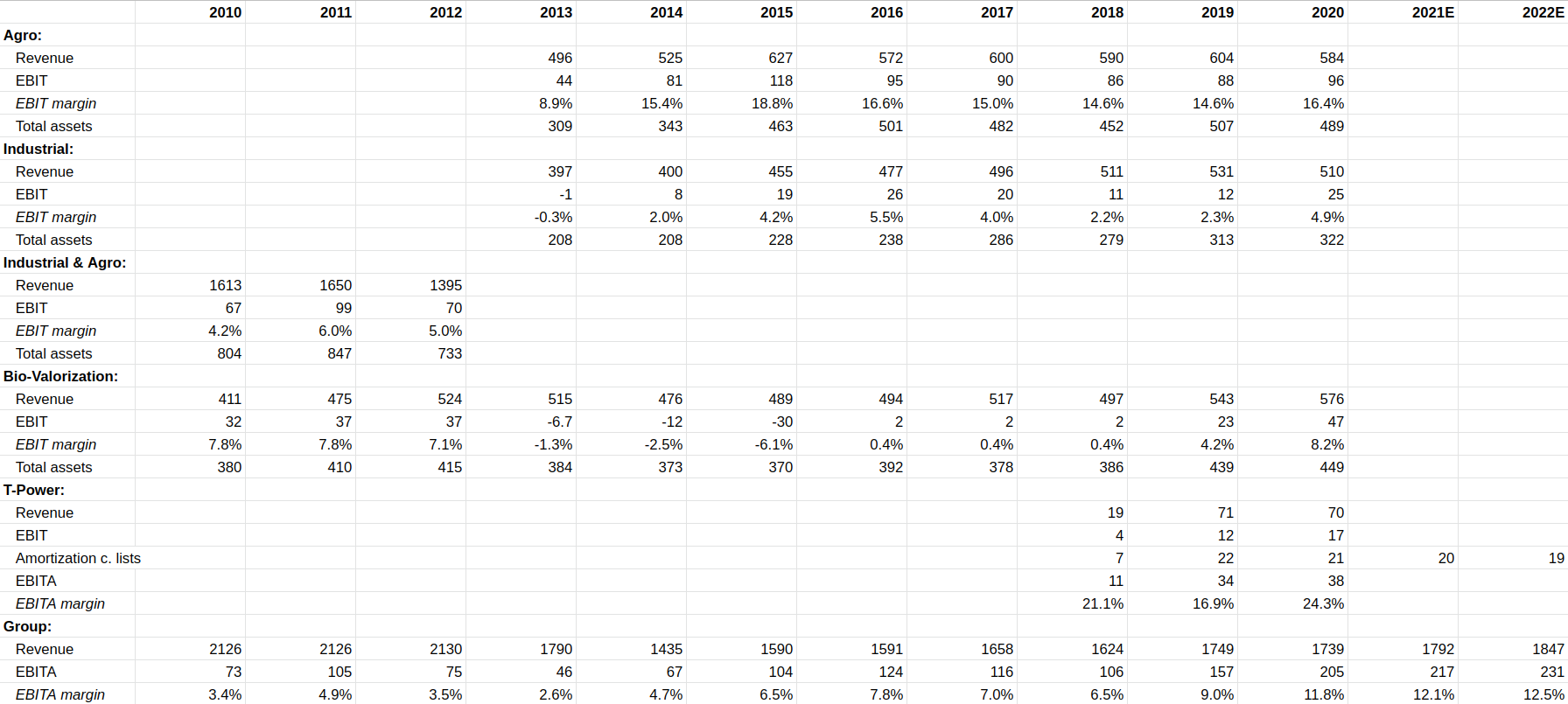

Picanol currently trades at €76 per share. A 30% CAGR in 12 years, not bad! I unfortunately was too late for this one, but was glad to find out he tried to do the same thing in 2013 by buying a large stake in Tessenderlo from the French government for €22 per share. The only problem is, profit did not really shoot up as expected as you can see below (click to enhance):

So I put this stock on my watch list, but kept an eye on it. And it appears it just took a bit longer this time around, as this business is likely more complex than Picanol. and it appears profit might increase significantly in the coming years. A strong indicator is that Luc Tack is not done buying yet, buying up nearly 1.5% of shares outstanding in one two transactions in June 2021 alone. Meanwhile the market is pricing this stock at 9x earnings and clearly thinks the 2020 increase in earnings was a one time bump. As historically this stock traded at 15-20x earnings, with arguably less attractive near term prospects.

Agro

Luc Tack is not your typical corporate raider. He cuts costs, but also reinvests in the business for the long run. This is made clear by looking at increase in assets in the above table. Supposedly the French government had underinvested in the business. They have recently reinvested and debottlenecked their fertilizer facilities in the US and are planning to build a major fertilizer plant in the Netherlands. If returns are the same as in the US, this could become a very attractive 15-20% ROIC growth business. This also appears to be a set of niche higher value add businesses as earnings are less volatile and returns are better than for example for CF industries, another fertilizer producer.

Additionally they could profit from the current agro boom. Produces like Corn, Wheat and Soya beans are at 7 year highs. Generally when prices are high farmers are willing to use more products to boost yields. So 2021 and 2022 might be very strong years for this segment.

Bio-Valorization

This is a animal by-product recycling business. It was humming along nicely, and when Tack took over, profits basically collapsed. They restructured and reinvested in this business in the past years and profits have shot up in 2020. Partially helped by market conditions as well. Management on how sustainable margins are on the H1 2020 call:

Stefaan Haspeslagh

In that respect, the -- it's difficult to make a difference between the various aspects. But basically, what we have been achieving is, through all our investments, we have been able to have more stable, more reliable factories, whereby we've been able to produce better qualities. And at the same time, we've introduced new products, which have created a higher value, both for us and for the customer. And at the same time, we have been debottlenecking factories.

So basically, the whole concept of reliability, better products, intrinsic products and also better-value products has led to the overall increase of sales of 8% over the total Bio-valorization business unit. It's very hard to say this is just a product, this is the value. This is hard to say. It's the total aspect, whereby mainly today, we are able to sell to customers who are more demanding and where we can meet their stricter demands.

And:

Stefaan Haspeslagh

It is a growing business, Mutlu. I can unfortunately, not on the top of my head, give you percentages what it means right now. But I can tell you it's moving up. Every half year, every quarter, we are able to attend better market, better customers with better products. It's an ongoing process.

Mutlu Gundogan

Yes. It sounds like a great business.

Stefaan Haspeslagh

It's a great business because every molecule counts. It's really what we are doing right from the beginning. And what we are doing is we told you for the last 3 years, we're investing in producing higher-value products and this is exactly what we have been doing.

Additionally Darling ingredients (mainly in the US) which appears to be in a similar line of business, and has followed a similar margin trajectory as Tessenderlo’s Bio-valorization segment, is expected to have significantly higher margins in the coming years:

So this might become a rather attractive growth business with ROIC already above 10%. At the very least it seems we are moving towards the better part of the cycle now.

Industrial

Their industrial segment mainly supplies pipes and chemicals for water treatment and chemicals to the mining and energy industry. This segment has been quite weak with subpar returns. Im not sure what to say about this. It does appear there is some cyclicality here. So if you are optimistic about mining and energy, this could become a nice business in the coming years. For now it is generating 7-8% returns in a good year. But is only a relatively small part of Tessenderlo’s income.

T-Power

Currently this is one gas power plant. It would seem like a boring low return business. But Tessenderlo purchased the other 80% in 2018 for €138 million. with an additional €190 million in debt. Net invested capital minus customer lists and not including debt, is €183 million. So ROIC is about 15% here, given that EBITA was about €38 million in 2020. They are planning to build another, bigger one for €500 million, which will be operational by 2025. Apparantly a major nuclear plant is overdue for closing, and the Belgian government, chaotic as they are, are struggling to replace this capacity. This comment by Skanjete on COBF nicely expands on why this could mean above average returns for Tessenderlo. A 10-15% ROIC would mean a €50-75 million increase in FCF from this new plant alone in 5 years.

So in conclusion it appears all their segments could have some nice tail winds over the next few years. Margins and overall ROIC could increase significantly in some of their business lines, and none of that is really priced in. FCF will likely be close to €200 million a year in the coming years, and the market cap is only €1.5 billion with close to zero debt by the end of this year. The reason it is cheap is probably because management is not very transparant and they are not making much effort to promote their stock, probably because Luc Tack wants to buy more shares more cheaply. And the market is likely skeptical that earnings increases can be sustained. Oh and because earning power is not immidiately obvious by glancing at the income statement.

Long at an average price of about €30 per share. And I may sell it at any time so DYOW.

Hey IJW, thanks for this writeup. Not sure where to leave my comments: twitter or here? So why not both?

Twitter: https://twitter.com/jefke00/status/1423217280247271424

Comments on TESB in general:

One of the frustrations with being an investor in TESB is that management refuses to give details in individual projects that would help you think about future earnings power / ROIC.

When asked about capex for a new fertilizer plant, they literally said "We don't give individual details on individual projects". They just guide overall capex for the full group and that's it.

Management doesn’t like to give a lot of guidance for the future. So investing in TESB for me is investing in a company cheap on current earnings/cash flows with optionality:

- not all current projects are "mature" (still some extra earnings to be squeezed out. "Continuously looking to de-bottleneck & increase production for existing locations")

- reopening will increase demand for some of their products

- they keep on investing in growth

Key words in the last couple of conference calls were:

Higher-value products: less of a commodity, higher margin/ROIC, less cyclical?

De-bottlenecking: not all plants running @ 100%: earnings can go up with limited extra capital invested

Specific comments on the article:

Bio-valorization

Comparison to Darling:

(keep in mind that TESB is downplaying all the time and doesn’t like to guide to optimistically / doesn’t guide over longer term than next year)

Analyst on cc has specifically asked about the bullishness of Darling & comparison to them:

They replied that the comparison isn’t perfect as Darling is more US focused, TESB more EU & Darling is the bigger, more mature player.

Mining & energy is only a small part of Industrial.

It’s basically 3 categories:

DYKA: plastic pipes

Chemicals for water treatment

Mining & energy (which also includes water treatment)

I have the impression mining & energy is something they don’t really focus on anymore.

No idea how “margins at maturity” can be for this segment. This is where we have trust that Tack knows what he’s doing and he wouldn’t be in this if he didn’t think he could squeeze more earnings out of the revenue in this segment.

T-Power

I see you adjust for the amortization of the customer lists. I think you can go a step further and think about depreciation. Details are a little fuzzy, but:

They earn € through a tolling agreement, independent of actual energy produced.

The power plant is running less than depreciation would indicate.

This agreement lasts until 2026. So at least until then, actual earnings are way higher than reported earnings. Not sure what happens after 2026.

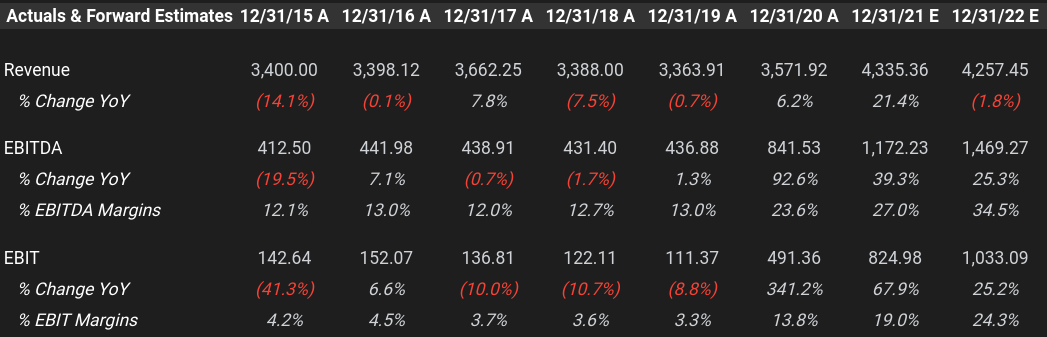

Valuation:

Last CC mgmt said “"We have about 100m FCF a year"... "after 100m investment and 100m repayment of loans"

Note that this investment includes growth capex. So actual current FCF is > 200m / year according to mgmt.

The real question is still how cyclical all these earnings actually are.

Thanks. I recommend reading equity valuation, both via DCF and relative valuation by Antoine Cloquet https://bit.ly/3fgLbXq

What is your opinion on owning Picanol for Tessenderlo exposure?